A Note on Agricultural Productivity in Latin America and the Caribbean: A Call to Increase Investment in Innovation

October 15, 2021

ARTICLE

By: Ruben G. Echeverria

Sr. Research Fellow at the International Food Policy Research Institute (IFPRI)

Director General Emeritus, International Center for Tropical Agriculture

Rural societies and agri-food systems in Latin America and the Caribbean (LAC) face common and unprecedented challenges such as: improving the efficiency of food and agricultural systems; increasing the sustainability of agriculture; building the resiliency of communities, agriculture, and ecosystems to adapt to climate change; and increasing economic and social inclusion, while contributing to opportunities for employment and income generation.

Innovation is critical to address such challenges. Therefore, technical and institutional change should be high on the agenda of policymakers, civil society, and the private and public sectors. Despite the development of agricultural innovation programs in the region during the past two decades, there is still a need to strengthen agricultural research, technology, and innovation systems (including digital innovation) to face such challenges. The LAC region offers an excellent opportunity to seek innovative, tangible, and large-scale rural development and agri-food systems results, particularly if it continues being the most significant net food exporting region (a challenge in terms of productivity), as well as maintaining its role as an essential provider of global environmental services such as biodiversity, water, soils, forests, and other ecosystem services.

Such challenges become even more relevant due to major global trends, such as changing consumer needs, climate change, low levels of public funding for agricultural research in the Global South, and the need to make agri-food systems healthier, sustainable, and more resilient. Furthermore, the severe overweight and obesity epidemic (combined with persistent hunger) in the LAC region and the mixed agricultural research and innovation capacity at the national level to respond to such challenges highlight the need to rethink how to innovate to realize impacts at scale.2

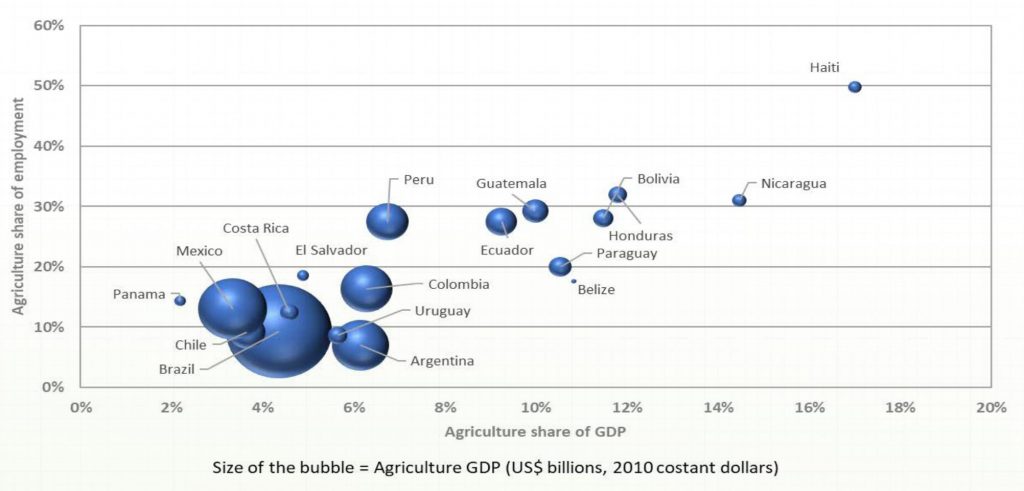

The current global technological innovation trends allow us to consider digital, data science, artificial intelligence, genomics, and new biological tools that can significantly improve agri-food systems and livelihoods. All these key challenges and opportunities for research, development, and innovation should be addressed considering the substantial heterogeneity of LAC countries, particularly regarding the diverse contribution of agriculture to economic growth and employment across countries (Figure 1.)

Figure 1: Contribution of Agriculture to GDP and Employment, LAC Countries, 2018

Source: World Bank, 2020. Future Foodscapes: Re-imagining agriculture in Latin America and the Caribbean

A critical dimension of heterogeneity for agricultural innovation in the region is that small-scale family farms are almost 85 percent of all farms. Of the approximately 15 million farms in the region, probably 13 million could be considered small-scale family farms. However, smallholder family farming is not a homogeneous sector. For example, a group of commercial family farms integrated into markets is already part of the science and technology innovation system. There is also a group in transition to commercial markets where technical assistance could play a key role. Finally, a more traditional or subsistence group of smallholders is not integrated into markets and is often marginalized from formal innovation systems and processes.3

INNOVATION AND PRODUCTIVITY

In the early 2000s, the performance of LAC’s agriculture sector was the best it had been in many years. This growth was short-lived. By the early 2010s, agricultural development was sluggish. The lesson is often repeated but remains true: only much more significant investment in research and development and innovation can sustain medium- and long-term improvements in productivity, sustainability and resilience, and social inclusion.

In 2000-2010, regional agricultural growth was strong, driven by a favorable macroeconomic environment and high prices for primary commodities. The sector saw a steady growth of total factor productivity (TFP), output and input per worker, and a reduction of the TFP gap between the region and OECD countries.4 Remarkably, even during the 2008 worldwide recession and the high phase of the commodity price cycle, some LAC countries were still increasing output per worker at an average annual rate of 4.4 percent between 2003 and 2012, compared with 0.7 percent in the 1980s.

The upward phase of the commodity price cycle that started in the early 2000s was over by 2011, with commodity prices falling or remaining stable, reflecting an anticipated increase in commodity supply along with weaker demand from China and other major commodity-importing economies.5 The past decade shows sluggish growth in several LAC countries, not only because of lower commodity prices but also because of macroeconomic difficulties and policy readjustments. Worsening fiscal conditions and a persistent increase in debt ratios brought back fiscal adjustments and recessions in the region.

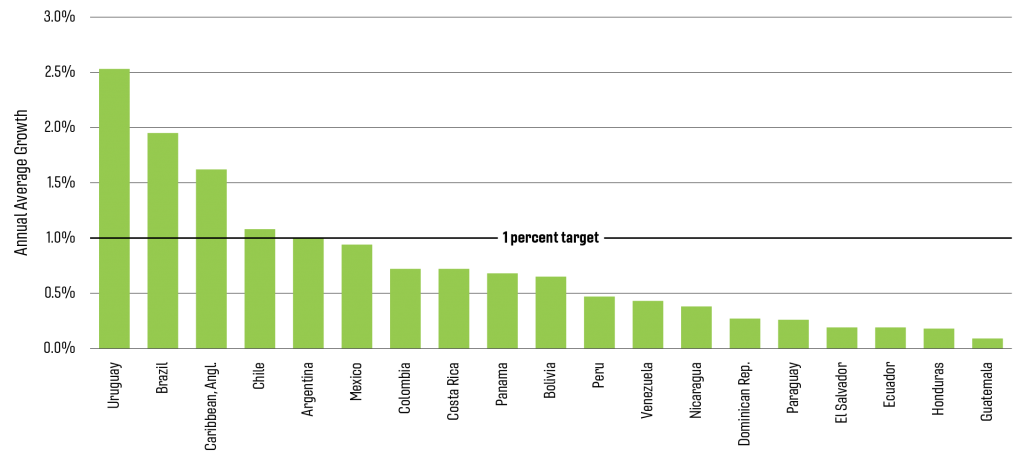

Regional agricultural growth decelerated after 2012. The average annual growth of output per worker between 2003 and 2011 was 4.4 percent, decreasing to 2.8 percent during 2012-2016. Output growth was driven almost equally by growth in TFP and input per worker. During the fast-growing period of 2003 to 2011, output growth was driven by TFP growth. TFP grew on average at an annual rate of 2.2 percent, the same as growth in input per worker. Regional agricultural growth decelerated after 2012. The average annual growth of output per worker between 2003 and 2011 was 4.4 percent, decreasing to 2.8 percent in 2012-2016. With the slowdown of production after 2012, TFP growth fell to an annual average of 1.3 percent, while growth in input per worker dropped to 1.5 percent. Although these growth rates are significant when compared to historic trends, the change signals the end of the favorable period for LAC’s agriculture.

TFP growth in agriculture was mainly driven by technical change, with average annual TFP growth rates of 2.2 percent during 2003-2011 and 1.1 percent after 2012. During the commodity price boom, crop and livestock production grew at an annual growth rate of 3.4 and 3.1 percent, respectively. TFP growth for both subsectors was slightly higher for crops (2.5 percent) than 2.2 percent for livestock. After 2011, annual growth in crop production dropped from 3.4 to 2.8 percent, and TFP decreased by half (from 2.5 to 1.2 percent). Growth rates of livestock output in 2012-2016 dropped to one-third of those in 2003-2011, from 3.1 to 1.0 percent, and TFP growth decreased from 2.2 to 0.7 percent. Livestock TFP seemed to reach a plateau after 2012, and crop production is the subsector driving growth.6

Greenhouse gas emissions increased much faster in crop production (3.4 percent) than in livestock production (0.8 percent), although emissions from livestock are six to eight times higher than crop emissions. Most of the emissions from agriculture come from enteric fermentation in ruminants and manure. In crop production, a primary source of emissions was synthetic fertilizer (more than half of the total emissions), rice cultivation, and crop residues. At the country level, between 2003 and 2011, Brazil, Paraguay and Uruguay were the countries with the fastest-growing agriculture, driven mainly by growth in crop production and the boom of soybean production for export, followed by Peru, Nicaragua, and Guatemala, all with agricultural production growth rates above 4 percent.7

THE NEED FOR MORE SIGNIFICANT INVESTMENT IN INNOVATION

There is no future for productive, sustainable, resilient, and inclusive agri-food systems in the region without a much greater commitment to investment in research, development, and innovation from the public sector, civil society organizations, and private companies. Investments in agricultural technologies in LAC are still relatively low, reaching only 1 percent of the venture capital investment in the region.8 As shown in Figure 2, only a few countries invest above 1 percent of agricultural production in research, compared with countries like China, Vietnam, and India that are investing over 2 percent of agricultural GDP in research and the higher income countries that have been continuously investing above 4 percent of agricultural GDP.

Furthermore, most of the research investment is focused on staple crops. Only a few countries have national research systems with high civil society participation and the private sector in the region.9 The public sector employed more than half of agricultural researchers in the mid-2000s, the higher education sector about 40 percent, and non-profit organizations 5 percent. However, there are significant variations across countries. For instance, in Brazil, the Dominican Republic, Ecuador, Panama, and Venezuela, the government sector employed more than 70 percent of each country’s agricultural researchers. In Mexico and Peru, roughly two-thirds of agricultural researchers were employed within higher education institutes. In Colombia and Honduras, producer organizations accounted for approximately 40 percent of the total number of researchers.

Figure 2: Agricultural Research Spending as a Share of AgGDP by Country, 2012–2016

Source: ASTI-IFPRI based on data from ASTI, OECD, RICYT, Embrapa, and Word Bank. Intensity ratios are for 2016 except for Ecuador (2014), Bolivia and Paraguay (2013), Anglophone Caribbean, Honduras, and Nicaragua (2012).

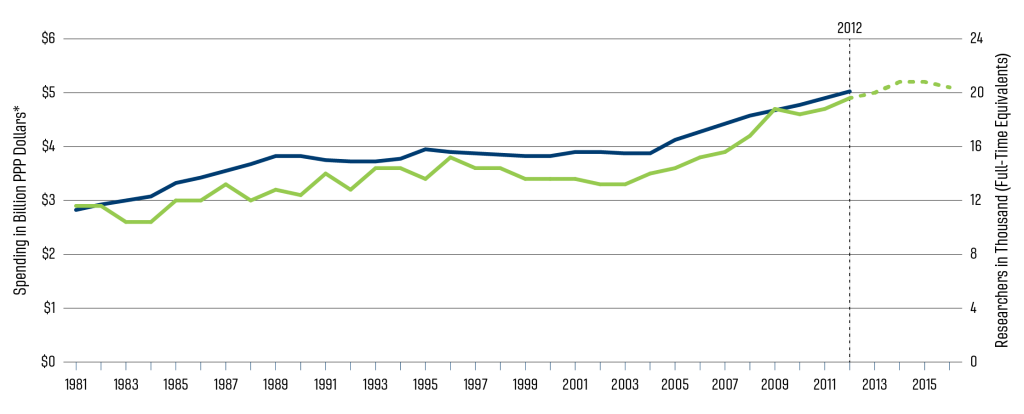

Figure 3: Total Number of Researchers and Agricultural Research Expenditures in LAC, 2016

*inflation=adjusted; 2011 prices. Source: ASTI-IFPRI based on data from ASTI, OECD, RICYT, and Embrapa. All researchers and research expenditures, excluding private companies. The 2014–2016 spending data for Argentina and Chile were updated using the OECD’s agricultural S&T spending trends; 2013–2016 spending data for Costa Rica, El Salvador, Guatemala, Panama, Peru, Uruguay, and Venezuela were updated using RICYT’s agricultural S&T spending trends; 2014–2016 data for Colombia and Mexico were estimated using RICYT’s general S&T spending trends; 2014–2016 spending data for Brazil were updated using Embrapa’s spending trends, and 2013–2016 spending trends were generated through a new ASTI survey round. All other countries were estimated using historical trends.

By 2016, the region invested about USD 5 billion annually in agri-cultural R&D (Figure 3), representing a significant increase over the previous decade. Total researcher numbers — measured in full-time equivalents – also increased to close to 20 000 agricultural researchers, nearly twice as many as in the early 1980s. Most of the growth in spending and number of researchers was driven mainly by the three countries with LAC’s most prominent agricultural research systems: Argentina, Brazil, and Mexico.

Considering the slowing down of growth in the agricultural sector during the past decade and the relatively low levels of investment in research, development, innovation, new partnerships, and financing mechanisms should be promoted by an endowment funded by several countries of the region and Spain. However, the current amount in the endowment (approximately USD 100 million) is still small to reach a significant regional scale. A unique institutional innovation was the creation, two decades ago, of the Regional Fund for Agriculture Technology (FONTAGRO) to support regional research projects on a competitive basis. The Fund operates with the income generated.

The region has benefited from the historical presence of relevant international agricultural research centers from the CGIAR based in LAC (CIAT, CIMMYT, and CIP) and others working in the region (Bioversity International, IFPRI, ICRAF as well as CATIE) with an important set of programs in the region. LAC has national research institutes with significant scientific capacities, including EMBRAPA in Brazil, INTA in Argentina, INIA in Uruguay and Chile, AgroSavia in Colombia, and INIFAP in Mexico. Furthermore, Universities, civil society organizations such as producer associations, and private companies have had a vital role in agricultural innovation in the region. Yet, despite these structures, LAC lags in terms of the level of investment compared with developed countries and other developing countries, most notably in Asia.

To complement publicly-funded activities, a key sector to promote — through institutional innovations and regulatory frameworks — is the private sector and civil society organizations such as producer associations. Private sector funded and executed research (focused on the primary sector and the rest of the innovation value chain, processing, marketing, and retail) is still at a low level in LAC compared to the rest of the world. Thus, in addition to significantly strengthening public-private partnerships, there is a need to improve coordination, complementarities, and synergies among all agricultural science, technology, and innovation agents.

In addition to increasing funding levels, it is crucial to rethink priorities and the new capacities needed in such systems. For instance, improving strategies, management processes, institutional evaluation, and organizational learning, planning, and business-related articulation for innovation, strengthening intellectual property regimes, and the capacity to develop start-ups and accelerators including government, businesses, and academia. In sum, promoting innovations to have a large-scale impact instead of simply for the generation and diffusion of technology should be prioritized.

Innovation is also required to identify ways to overcome the most common barriers to adopting new technologies. In this regard, sound policies could incentivize much-needed investments in research, technology development, and innovation. According to global assessments, these barriers include training and information (88 percent), policy/institutional (39 percent), economic (30 percent), social/cultural (16 percent), and environmental (9 percent).10 Specific barriers to technology adoption include low availability of required inputs (such as high yielding seeds for improved varieties or water scarcity during droughts), high costs of installation (e.g., enhanced irrigation facilities) with limited access to credit and markets, high labor costs and a limited level of technical knowledge and skills. Strengthening social networks among producers to share initiatives, good practices, and innovations is critical in this regard.

Endnotes

Based on Echeverria, R.G. 2020. Innovation for sustainable, healthy, and inclusive agrifood systems and rural societies in Latin America and the Caribbean. Framework for action 2021-2025. Food and Agriculture Organization of the United Nations, Regional Office for Latin America and the Caribbean. FAO, Santiago de Chile.

For a recent comprehensive review of agrifood systems in the region, see Díaz-Bonilla, E. and R.G. Echeverría (2020). Duality, urbanization, and modernization of agri-food systems in Latin America and the Caribbean. In K. Otsuka and S. Fan (eds.) World Development. New Perspectives in a Changing World. IFPRI: Washington DC.

Berdegué, J. & Fuentealba, R. 2011. Latin America: The State of Smallholders in Agriculture. IFAD, Rome.

Nin-Pratt, A., Falconi, C., Ludena, C.E. & Martel, P. 2015. Productivity and the Performance of Agriculture in Latin America and the Caribbean: From the Lost Decade to the Commodity Boom. IDB Working Paper Series. Inter-American Development Bank. Washington DC.

Nin-Pratt, A. & Falconi, C.A. 2019. Agricultural R&D Investment, Knowledge Stocks and Productivity .rowth in Latin America and the Caribbean. IFPRI Discussion Paper 01730. Washington DC.

Parra-Peña, R.I. et al. 2021 (Una hoja de ruta para el aumento de la productividad agropecuaria de Colombia: desafíos y oportunidades. Fedesarrollo, Colombia) show a 0.6% annual growth rate of agricultural total factor productivity in Colombia for 2001-2016, one of the lowest in the region (1.8% average during that period according to the author). Similar low productivity figures for Colombia are reported for agricultural labor productivity for the same period, with an estimated average value added per farm worker of $5,086 (2010 constant dollars) compared with a $5,990 average for the region. Although those figures represent less than 7 per cent of the US farm labor productivity they are close to Mexico’s figures ($5,107) and higher than Argentina’s ($2,809) and Peru’s ($2,184) although lower than Chile ($9,266) and Brazil ($7,661).

During the period 2012-2016, only one country shows an average growth rate of 4.0 % (Guatemala), followed by Bolivia (3.8 %), Mexico (3.1 %) and Dominican Republic (2.9 %). The fastest growing countries in the earlier period are now growing at rates of 2.4 % (Paraguay), 1.1 % (Brazil) and 0.3 % (Uruguay). Crop production continues to be the fastest growing subsector in the fastest growing countries, with growth rates of 4.6 % in Guatemala, 5.4 % in Bolivia, 5.4 % in Mexico and 4.7 % in Dominican Republic. (Nin-Pratt and Falconi, 2019)

Gert-Jan Stads, N. Beintema, S. Perez, K. Flaherty and C. Falconi, 2016. Agricultural Research in Latin America and the Caribbean. A cross-country analysis of institutions, investment, and capacities. ASTI and IDB, Washington DC.

World Bank, CIAT, CGIAR & CCAFS. 2018. Bringing the Concept of Climate-Smart Agriculture to Life: Insights from CSA Country Profiles across Africa, Asia, and Latin America. World Bank. http://ciat.cgiar.org/wp-content/uploads/COP_CSA_Synthesis_ToPrint.pdf

Partner Case Study:

Partner Name

Close

Chellie Maples, Ph.D

Dr. Chellie Maples is an agricultural economist focused on advancing sustainable productivity growth and strengthening the economic resilience of agricultural systems. Her work centers on agricultural productivity growth and decision-making across farm, industry, and policy levels, with an emphasis on translating rigorous research into actionable insights for producers, policymakers, and industry stakeholders.

In her current role, Dr. Maples contributes to advancing the mission of the Global Agricultural Productivity Initiative by supporting the development of the annual GAP Report and leading an economic research portfolio that informs global discussions on agricultural productivity growth, applying econometric and quantitative methods to generate credible, decision-ready insights. Her work focuses on identifying pathways to close agricultural productivity gaps.

Dr. Maples has extensive experience synthesizing research and communicating findings to diverse audiences. She has translated complex production economics literature into practical resources—including presentations, white papers, and producer-facing guides—designed to support real-world decision-making. Through this work, she has developed a strong ability to bridge the gap between research and application, ensuring that technical insights are accessible, relevant, and usable across stakeholder groups.

Dr. Maples holds a PhD in Agricultural Economics from Oklahoma State University and a Master of Science in Agricultural Economics from Mississippi State University.

In her work, she collaborates across disciplines and sectors to advance data-driven, economically sound approaches to improving agricultural productivity and resilience.

Hannah Dredger is a junior majoring in Ecological Restoration with minors in Global Food Security and Health and Biodiversity Conservation. She is interested in sustainable agriculture, land conservation, and food security, and how ecological practices can strengthen global food systems. She has been a CALS Global/GAP Initiative intern since June 2025 and hopes to pursue a career focused on conservation-driven solutions to food security challenges.

Spring Ashby, MPA, is a strategic communications and engagement leader who turns complex data into clear, actionable insights that drive engagement and decision-making. As Communications Manager for the GAP Initiative at Virginia Tech, she leads messaging, digital strategy, and stakeholder engagement to strengthen how agricultural productivity data is communicated and used across global audiences.

Raised on a working farm, Spring brings a personal and practical understanding of agriculture and livestock production to her work, grounding her communications approach in the real-world challenges and opportunities facing producers. She pairs real-world agricultural experience with a data-informed approach, using clear messaging and focused campaigns to drive engagement and expand reach.

In her previous role with Virginia Cooperative Extension, she led multi-channel outreach for more than 2,500 annual participants and contributed to 340% program growth through strategic messaging, audience targeting, and campaign execution. She managed communications across partners, led high-impact events and campaigns, and secured grants, sponsorships, and endowment funding to expand access to 4-H positive youth development education in Frederick County and Winchester City, Virginia.

Her current work sits at the intersection of strategy, storytelling, and operations. Ensuring that communications efforts are not only compelling, but measurable and effective. Spring Ashby holds a Master of Public Administration from Virginia Tech and a Bachelor of Science in Dairy Science, with minors in Horticulture and Equine and Animal Sciences.

Madison serves as Communications Manager for the GAP Initiative. Her responsibilities include design and production of the annual GAP Report, strategic communications and media relations to grow the influence of the GAP Initiative, and collaboration with more than 20 GAP partner organizations worldwide.

Madison brings with her diverse experience across the food system. Before joining the CALS Global team, she advocated for global food security policy on Capitol Hill and managed a $2 million grant program to connect farmers across 5 states to resources provided by USDA-NRCS. Madison is a proud Hokie; she holds a B.S. from Virginia Tech in Sociology and Political Science (2019). During her undergraduate studies, she participated in experiential learning in Rwanda to conduct focus groups on local public health needs, school feeding programs, and smallholder farming initiatives.

Dr. Tebila Nakelse serves as the GAP Initiative Research Lead for the Global Agricultural Productivity Initiative, leading the research and analysis agenda for the annual GAP Report. Originally from Burkina Faso, he earned his Ph.D. in Agricultural Economics at Kansas State University. His prior roles include working at UN-FAO as a Policy Specialist and Senior Policy Advisor, and positions at the Tony Blair Institute for Global Change and the Africa Rice Center.

Tebila has extensive experience in various countries including the US, UK, Italy, Benin, Cote d’Ivoire, and Burkina Faso. He will bring his significant expertise in agricultural productivity and policy to the GAP Initiative, linking the GAP Report with vital food and public policy issues.

Dr. Jessica Agnew is a global food systems expert dedicated to advancing equitable, resilient agri-food systems and improving access to nutritious foods worldwide. As Managing Editor of the Global Agricultural Productivity (GAP) Report at Virginia Tech and co-lead of the GAP Initiative, she develops and executes strategies to drive investment and action in agricultural productivity growth to meet the world’s evolving agricultural needs. In her concurrent role as Associate Director of CALS Global, she leads initiatives to internationalize the talents of faculty and students in the College of Agriculture and Life Sciences (CALS).

Drawing from her background as a former chef, Dr. Agnew brings a unique perspective to her research portfolio. Her research focuses on innovative approaches to making nutrient-rich foods more accessible to low-income populations and strengthening agri-food value chains through digital technologies, with a particular focus on blockchain applications in Kenyan agriculture. She has led international research projects, including a USAID-funded study on blockchain technology’s potential to improve food security through African Indigenous Vegetables in Western Kenya.

Dr. Agnew holds a PhD in Planning, Governance, and Globalization and a Master of Public Health from Virginia Tech, along with master’s and bachelor’s degrees in Food, Agriculture and Resource Economics from the University of Guelph. Her doctoral research explored market-based approaches to addressing micronutrient malnutrition in Mozambique, reflecting her commitment to finding practical solutions to global nutrition challenges.

In her current work, she collaborates with a vibrant global community to create meaningful impact in food systems, environmental sustainability, economic development, and public health. Her expertise spans market-based nutrition solutions, agricultural innovation.

Thomas L. (Tom) Thompson is Associate Dean and Director of CALS Global in the College of Agriculture and Life Sciences at Virginia Tech. CALS Global builds partnerships, drives thought leadership, and creates opportunities for students and faculty to serve globally.

Thompson earned BS, MS, and PhD degrees in agronomy and soil science. He was department head at Virginia Tech (2011-16) and Texas Tech University (2006-11) and professor and extension specialist at the University of Arizona from 1991 to 2006. Thompson is also Professor of Agronomy and has published more than 65 refereed journal articles and garnered more than $18 million in competitive funding and philanthropic support. His recent research and outreach have focused on adoption of conservation agriculture in smallholder farming systems in Haiti, Senegal, and Southeast Asia. He has mentored graduate students from Africa, Asia, and Central and South America.

He has been Executive Editor of the Global Agricultural Productivity Report (GAP Report) since 2019. The annual GAP Report is a thought leader in agricultural productivity and benefits from partnerships with agricultural industry leaders, conservation and nutrition organizations, and NGOs. The GAP Report is launched at the annual World Food Prize event in Des Moines, Iowa. He is a Fellow of the American Society of Agronomy, the Soil Science Society of America, LEAD21, and the Food Systems Leadership Institute.

Paul Spencer joined Corteva Agriscience in January 2019 and is the Global Trade Policy Advocacy Leader. He provides strategic counsel to the company’s business platforms on a range of trade policy issues, including plant breeding innovations, biotechnology asynchronous approvals, low-level presence, and pesticide maximum residue levels.

Paul represents Corteva externally on the the U.S. Grains Council’s Trade Policy Advisory Team, the National Grain and Feed Association’s Crop Technology Committee and the CropLife America Trade Steering Group. He is currently the Chairman of the BIO Innovation Organization’s Agriculture International Working Group. Mr. Spencer began his career with the Department of Agriculture in 1993. From 2010-14, he was Agricultural Counselor at the U.S. Embassy in Berlin and was responsible for USDA programs and policies in Austria, Hungary, and Germany. He has also served at U.S. Embassies in Baghdad, Tokyo, and Vienna.

Mr. Spencer holds an MBA in International Business from the Thunderbird School of Global Management and a degree in Economics from Colorado State University. He is married to Sandy MacGregor and they have three children, Grace, Forrest, and John.

Brady Deaton

Brady J. Deaton was Chancellor of the University of Missouri 2004-2013 and now serves in emeritus status and as Director of the Deaton Institute for University Leadership in International Development at Missouri. He was appointed Chair of BIFAD by President Obama in 2011 and reappointed to a four-year term as a member of BIFAD in January 2016-2020 by President Obama.

He has worked in many countries to strengthen their capacity for agricultural and economic development, and has received three honorary degrees from universities in Thailand and Korea, and an Honorary Doctorate from the University of Kentucky. He was elected to the Missouri Cooperatives Hall of Fame. In 2014, he received the Missourian Award and in 2015 was named to the Alumni Hall of Fame of the University of Kentucky.

Deaton served as chair of the Academic Affairs Council of the Association of Public and Land-grant Universities (APLU) and participates in advisory roles with the U.S. Department of Agriculture. He completed a two-year term as chair of the Missouri Council on Public Higher Education and was chair of the Big 12 Conference Board of Directors. He served as a Board member of the National Foundation of Credit Counselors and is currently a Board member of the Online Computer Library Center (OCLC) and Board member of the Soybean Innovation Lab.

He is a recipient of the Malone Award from the APLU for furthering international education in public higher education, was a member of the board of the Donald Danforth Plant Science Center throughout his time as Chancellor, and served on the International Committee of the Association of American Universities (AAU). During April, 2014 and in 2015, Deaton served as a “Distinguished Guest in Residence” at New York University.

Alexis Taylor

Alexis Taylor is an Iowa native, with a career focused on U.S. agricultural and trade policy. Prior to her appointment as Under Secretary for Trade and Foreign Agricultural Affairs, Alexis was appointed by Oregon Governor Kate Brown as director of the Oregon Department of Agriculture (ODA) in December 2016. As director, she worked to promote and regulate agriculture and food, keeping the mission to ensure healthy natural resources, environment, and economy for Oregonians now and into the future at the forefront.

Prior to Alexis’ appointment, she oversaw the U.S. Department of Agriculture’s (USDA) Farm and Foreign Agricultural Services (FFAS). While traveling the world she worked to open new markets and improve the competitive position of U.S. agricultural products in the marketplace. Before joining USDA, Alexis worked for several U.S. Congressman, staffing members from Montana and her home state.

Alexis is a graduate of Iowa State University and grew up on her family farm in Iowa, which has been in her family for 160 years. While still in high school, she enlisted in the U.S. Army Reserves. During her junior year in college her army unit was deployed to Iraq, where she served one tour with the 389th Combat Engineer Battalion. While no longer an active reservist, Alexis continues to advocate for veterans.

Eugenia Saini

Eugenia Saini is currently FONTAGRO’s Executive Secretary. FONTAGRO is the Regional Fund for Agricultural Technology. She leads the investment fund and a portfolio of 70 international operations related to science, technology, and innovation for the Latin America and the Caribbean region. She is from Argentina and is an agronomist by training. She holds a doctorate in agricultural sciences, specializing in total factor productivity analysis. One of her seminal works in this field was the estimation of 120 years of TFP for the agricultural sector in Argentina. She is also a National Public Accountant and holds an MS in Food and Agribusiness and an MS in Applied Economics, both from Universidad de Buenos Aires. She has worked in the private and public sectors, both nationally and internationally, especially in multilateral banks. She was awarded a Fulbright Scholarship at Cornell University and, more recently, with the Abshire-Inamori Leadership Academy (AILA) Scholarship at the Center for Strategic & International Studies (CSIS) in Washington, D.C.

Sergio Rivas

With a background in industrial engineering and economic development, Sergio Rivas began his career in international development 22 years ago. His work in the industry includes roles as Contracts Officer Representative, Senior Director, Chief of Party, Country Representative, Board Member, donor, and volunteer on both public and private sector engagements.

For the past 15 years, Rivas has worked for Tanager’s parent company, ACDI/VOCA, in various senior leadership roles, most recently as Regional Managing Director in Honduras. From 2012-2016 he served as Tanager’s Country Representative in Colombia where he got to know the organization, developing an enormous admiration for its work, its people, and its clients.

Rivas assumed the role of President of Tanager in 2022.

Adam van Opzeeland

Adam van Opzeeland has served as New Zealand’s First Secretary for Agriculture Trade to the United States since July 2022. His responsibilities include managing the bilateral agriculture policy relationship, working with US counterparts to facilitate the bilateral trade of agriculture goods, and collaborating with the US and other partners to advance common agriculture and trade objectives in regional and multilateral fora. Prior to this role, Adam spent eight years representing the New Zealand Government in Free Trade Agreement negotiations and as a delegate to a range of United Nations Conventions and Organizations. He holds a Master’s Degree in Sustainable Development from the University of Queensland.

Ruramiso Mashumba

Ruramiso Mashumba is a young female farmer from Marondera, Zimbabwe, and founder of Mnandi Africa, an organization that helps rural women combat poverty and malnutrition. She holds a BA Degree in Agriculture Business Management from the University of West England (UWE). Postgraduate Diploma in Management from Regent University, South Africa. She Is currently studying for an MBA in sustainable food and agriculture at the Royal Agriculture University in Cirencester, UK.

Rosalind R. Leeck

Rosalind (Roz) Leeck is the Executive Director for Market Access and Strategy as well as Northeast Asia Regional Director at the U.S. Soybean Export Council. She oversees strategic program development and implementation including trade and market access issues; membership and industry relations; and communications and marketing efforts. She is also the Regional Director for Northeast Asia responsible for Korea and Japan.

Roz has more than 10 years of experience in the grain trade field with previous positions at Archer Daniels Midland Co. and Demeter L.P. She has also worked for Indiana Corn Marketing Council (ICMC), Indiana Soybean Alliance (ISA), and the Indiana State Department of Agriculture.

Roz has been involved in a number of industry activities and is currently serving on the Management Council of the International Grain Trade Coalition and as a cleared advisor and vice chair for the USDA and USTR Agricultural Technical Advisory Committee for Trade in Grains, Feeds, Oilseeds, and Planting Seeds. Additionally, she serves on the Board of Trustees at Millikin University. Roz originally hails from southern Illinois where she remains a partner in her family’s grain and livestock farm. She earned a Bachelor of Science Degree in Economics from Millikin University in Decatur, Illinois, a Master of Business Administration from Butler University in Indianapolis, Indiana and a Master of Science in Agricultural Economics from Purdue University in West Lafayette, Indiana.

Chris Davison

Chris is the President & Chief Executive Officer of the Canola Council of Canada.He is responsible for leading the efforts of the Council’s professional staff and reporting to the Board of Directors on securing the key objectives of the Canadian canola industry.

Chris firstjoined the Council in August 2021 as Vice President, Stakeholder and Industry Relations. Prior to joining the Council, Chris spent nearly 10 years with a global life sciences company serving as Head of Business Sustainability for North America and prior to that Head of Corporate Affairs for Canada.

Chris also spent several years on the consulting side of the agri-food industry working in government and industry relations, corporate communications and public affairs to advance issues and opportunities at the global, regional, national and sub-national levels for a diverse set of private sector and association clients.

Earlier in his career, Chris worked for the Canadian federal government on animal health, plant health, and food safety related issues in support of Canadian bilateral and multilateral trade relationships and negotiations.

Saharah Moon Chapotin

Dr. Saharah Moon Chapotin joined the Foundation for Food & Agriculture Research (FFAR) as the executive director in August 2022.

Chapotin is a plant scientist who is passionate about sharing the importance of plants and agriculture. She has more than 15 years of experience in federal leadership, using science to inform policy and advancing agriculture research. Most recently, Chapotin served as the executive director of the United States Botanic Garden (USBG), a position she held from 2018 to 2022.

Prior to her role at USBG, Chapotin worked at the United States Department of Agriculture and the United States Agency for International Development (USAID) for over 11 years. She held multiple positions at USAID, serving as the deputy assistant administrator in USAID’s Bureau for Food Security. Earlier in her career, Chapotin completed fellowships at Iowa State University and the National Academies working on issues of biosafety policy, scientific communication and national security. She further conducted research on forest ecology and canopy biology throughout the United States, Madagascar and Costa Rica.

Chapotin holds a bachelor’s degree in biology from Stanford University and a doctorate in plant physiology from Harvard University.

Dan Blaustein-Rejto Bio

Dan Blaustein-Rejto is the Director of Food & Agriculture at the Breakthrough Institute where he leads work examining how public policy can support environmentally and socially beneficial innovation across the food system. Dan has led multi-stakeholder projects to identify technical options to decarbonize agriculture, assess federal policy gaps and opportunities, and build coalitions to advance climate-smart agriculture. Dan has written for Foreign Policy and MIT Technology Review, among other publications. He and his work have been cited in Bloomberg, LA Times, Agri-Pulse, Beef Magazine, and other outlets.

Dr. Tek B Sapkota

Tek Sapkota Leads the Climate Change Science group in CIMMYT and is a member of the Climate Investment Committee in OneCGIAR. His research interest includes analysis of cropping systems from food security climate change nexus. He is involved in studying management consequences on nutrient dynamics in agro-ecosystem and their effect on food security, climate change adaptation and mitigation. He has served in IPCC as Lead author as well as Review editor. He is an associate Editor of “Nature Scientific Report” and “Frontiers in Sustainable Food Systems” journals. He is an Agricultural expert in the “India GHG platform” (http://ghgplatform-india.org/).

Paul JG Rennie OBE

Paul Rennie was born in Edinburgh and educated at George Heriot’s School, before going on to graduate with an MA in Economics and Politics (Edinburgh University) and an MSc in Economics (York University). He joined the Foreign and Commonwealth Office in 2001 as the first of a new group of Diplomatic Service Economists. He has served at the United Nations (New York), Brazil, India and Malaysia, as well as working on secondment to the Cabinet Office and the Department for International Development. Paul currently serves as the Counsellor for the Global Issues, Economics and Trade Section at the British Embassy, Washington DC. Here he leads the UK’s climate and energy, economic and trade, and science and technology networks across the United States. Paul also speaks five languages (English, French, Dutch, Portuguese and Hindi)!

Christina Zola Peck

Christina is a seasoned communications professional with over 30 years’ experience, including 14 in international development. Her background in business development, communications and public relations fully informs her strategic communications initiatives at IFDC.

As Strategic Communications Manager for IFDC, she regularly collaborates with IFDC’s international project staff, partners, and donors to design and implement evidence-based strategic communications campaigns. She tells big stories about the Center’s work in soil health and plant nutrition, inclusive market systems, and innovative technologies for a food-secure and environmentally sustainable world.

Prior to joining IFDC, Christina was with the National Cooperative Business Association CLUSA International (NCBA CLUSA), serving as a technical writer and proposal manager in their International Division. As communications manager at Making Cents International, she developed and implemented project-level communications strategies, especially regarding youth development activities under USAID’s flagship YouthPower Learning project. While at URC as a communications specialist, she developed, executed, and monitored communications strategies to support corporate and project objectives, including creating and facilitating #GBVChat, an annual all-day conversation about ending gender-based violence that engaged 10,000+ unique participants in its first year, while standing up the organization’s social media platforms and story-telling strategies.

As Director of Communications at the Arab American Institute, she created and executed strategies for long-term advocacy as well as for fast-breaking crisis situations, including a daily analysis of the Gaza War (Operation Cast Lead) for media and AAI membership.

Pierre Petelle

Pierre Petelle is the president and CEO of CropLife Canada, the trade association that represents the Canadian manufacturers, developers and distributors of pest control products and plants with novel traits. Pierre joined CropLife Canada in 2008 and is now responsible for the strategic direction and leadership of the association.

CropLife Canada’s goals include improving public confidence in our members’ technologies, facilitating a positive regulatory environment, ensuring proper stewardship of our industry’s products and building collaborative stakeholder relationships.

Prior to joining CropLife Canada, Pierre worked in the policy office at Health Canada’s Pest Management Regulatory Agency where he worked on a wide range of issues relevant to Canada’s plant science industry. Pierre holds degrees from Carleton University and the University of Guelph.

Matthew Worrell

Matthew Worrell currently represents Australia’s agriculture interests in the United States and works with colleagues in the Australian High Commission in Ottawa to progress bilateral agriculture issues with Canada. Matt has extensive experience in agriculture policy development and implementation, and international representation. Matt was based in Europe from 2012 to 2016 where he represented Australia’s interests at the United Nations Food and Agriculture Organization and the Organisation for Economic Co–operation and Development. Matt holds a bachelor’s degree in agricultural economics from the University of New England and a master’s degree in public policy from the Crawford School of Public Policy at the Australian National University.

Nikki Dutta, M.S.

Nikki Dutta, M.S., scientific program officer, advanced animal systems, Foundation for Food and Agriculture Research. At the Foundation for Food and Agriculture Research (FFAR), Ms. Nikki Dutta, is responsible for coordinating several multi- stakeholder collaborative initiatives designed to improve animal welfare and productivity, including the Greener Cattle Initiative, Egg- Tech Prize and the International Consortium for Antimicrobial Stewardship. Nikki earned her master’s degree from American University in sustainability management and studied international business and management at Dickinson College.

Sarah Brown

Sarah Brown serves as Head of Public Governmental Affairs Agricultural Solutions North America, based in Washington, DC. Sarah previously served as an Executive Director for the American Farm Bureau Federation. Sarah is a graduate of Cornell University, where she currently serves on an advisory board for the College of Agriculture and Life Sciences.

François Chrétien

Mr. François Chrétien received his bachelor of sciences in agriculture from McGill University and his master’s degree in Water Sciences from the National Institute of Scientific Research. Following is graduated studies he has been involved in numerous water-focused initiatives throughout Canada and around the world. Within Agriculture and Agri-Food Canada he served as: Water Sourcing and Planning Specialist; Water Management Scientist; Chief of the water management team; before moving on to executive management as Director for Agriculture and Agri-Food Canada’s (AAFC) living labs.

Since 2017, François has been responsible for the development of AAFC’s Living Laboratories Initiative aimed at building resilience in the agricultural landscape. François was also central to the development and implementation of AAFC’s new program, the Agricultural Climate Solutions program, that is establishing a national network of living labs right across Canada to tackle climate change issues. He has worked with multiple Canadian and international partners in order to develop this new approach to agricultural innovation, including the G20 working group on Agroecosystems living labs. Under François leadership, Canada has been paving the way to implement this user-centred approach where farmers and scientists work together from start to finish; where transdisciplinary teams, including experts from various disciplines and backgrounds, tackle a common issue together; and where projects are conducted in real life experimental setups meaning that working farms are the incubators of innovative technologies.

François has real, tangible experience in developing innovative solutions for a productive, sustainable and resilient agriculture sector.

Jocelyn Brown Hall

Jocelyn Brown Hall is the Director of the Food and Agriculture Organization of the United Nations (FAO) Liaison Office for North America based in Washington, DC. Prior to this role she served as the Deputy Regional Representative for the FAO Regional Office for Africa, where she oversaw 47 FAO country offices and guided strategy and communications around food security, agriculture, climate change, agrifood trade, animal and plant health, among other topics. She has also served as the FAO Representative for Ghana, where she worked with ministries of agriculture, fisheries, social protection and trade on advancing issues such as healthy school meals, rehabilitating lands contaminated by illegal mining, sustainable aquaculture and fish smoking, and digitalization of agriculture data.

Before joining FAO, Jocelyn was Deputy Administrator in the Foreign Agricultural Service, where she led the USDA’s USD $2 billion food and technical assistance programs in low- and middle-income countries. She oversaw the world’s largest international school meals program, serving over 4 million school children globally, and numerous fellowship programs that served tens and thousands of agriculturalists.

She also served as the lead expert on USDA’s technical relationship with international organizations such as the Food and Agriculture Organization of the United Nations, the Inter-American Institute for Cooperation in Agriculture, and various international research centers.

Dr. Elise Golan

Dr. Elise H. Golan is the Director for Sustainable Development at the U. S. Department of Agriculture. In this role, she provides leadership in planning, coordinating, and analyzing the Department’s policies and programs related to sustainable agricultural development. Prior to taking this position, Dr. Golan served as the Associate Director of the Food Economics Division at the Economic Research Service, USDA. Before joining USDA, she did consulting work for, among others, the World Bank, the International Labor Organization, and the California Department of Finance. Elise served as a senior staff economist on the President’s Council of Economic Advisers from 1998-99. She received her Ph.D. in agricultural economics from the University of California at Berkeley. Dr. Golan’s research has spanned a wide range of sustainability issues, including land tenure and sustainable land management in the Sahel and West Africa; regional and U.S. food-system modeling; food labeling and market development; food access, affordability, and security; and the distributional consequences of food policy.

Keith Fuglie

Keith Fuglie is a senior economist with the Economic Research Service, U.S. Department of Agriculture, where he conducts research on the economics of technological change and science policy for agriculture. While with the Federal Government, Keith has also worked at the U.S. Agency for International Development’s Bureau of Food Security and served as senior staff economist for the White House Council of Economic Advisors. In 2012 Keith was recognized with the USDA Secretary’s Honor Award for Professional Service, and in 2014 he received the Bruce Gardner Memorial Prize for Applied Policy Analysis from the Agricultural and Applied Economics Association. Earlier in his career, Keith spent ten years with the International Potato Center (CIP) stationed in Indonesia and Tunisia, where he headed CIP’s social science research program and was regional representative for CIP in Asia. Keith received his M.S. and PhD in Agricultural and Applied Economics from the University of Minnesota and a BA from Concordia College, Moorhead, Minnesota.

Robert Fries

Bob Fries is chief technical officer, overseeing our technical teams as they develop programmatic approaches, share best practices and technical products with projects overseas, and apply evidence to optimize the effectiveness and impact of our work. Bob is also president of AV Ventures, ACDI/VOCA’s subsidiary dedicated to blended finance and impact investment. He has engaged in the design and governance of 10 financial institutions affiliated with ACDI/VOCA, including AV Ventures. Prior to joining ACDI/VOCA in 1989, Bob was a volunteer in Belize and researcher of seasonal labor migration in Guatemala. He holds a bachelor’s degree in political science from Boston College and a master’s degree in economic and social development from the University of Pittsburgh. Bob is proficient in Spanish and has contributed to Value Chains and Their Significance for Addressing the Rural Finance Challenge and Nature-Centered Tourism in Ecuador, published by USAID, Basic Guidelines for Effective Rural Finance Projects, published by the World Bank, and Making Rural Financial Institutions Sustainable, published by the United States Department of Agriculture.

Dr. Canisius Kanangire

Dr. Canisius Kanangire is the Executive Director at AATF. He previously was the Executive Secretary of the African Ministers’ Council on Water. He has held other positions including, Executive Secretary of the Lake Victoria Basin Commission; Regional Manager for Capacity Building and Head of Strategic Planning and Management at the Nile Basin Initiative; Lecturer and Dean – Faculty of Agriculture, University of Rwanda.

He holds a PhD and MSc in Aquatic Sciences from the University of Namur (Belgium), a Degree in Biology majoring in Environmental Sciences, and an Undergraduate Certificate in Biology and Chemistry from the “Institut Supérieur Pédagogique de Bukavu.

Andrés Rodríguez

Andrés Rodríguez is the current Agricultural Attaché of Chile to the United States and Canada, based in Washington DC.

He holds a Bachelor’s Degree in Business from Diego Portales University (Chile), a Master’s Degree in Marketing from Griffith University (Queensland, Australia), and a Postgraduate Certificate in International Business from the University of Chile.

He has extensive experience in agribusiness. After his experience in other industries, he landed to the agriculture when he was appointed as Marketing Manager for the US and Latin America in the Chilean Fresh Fruit Exporters Association (ASOEX). Within his background he also was Executive Director of the Chilean Walnut Commission, Executive Director of Chile Prunes, and Representative in Chile of the Produce Marketing Association (PMA), that currently is the International Fresh Produce Association. He was also Board Member and Counselor of the National Society of Agriculture (SNA) and was a member of the Food Export Council of Chile.

Stewart Leeth

Stewart Leeth is chief sustainability officer for Smithfield Foods, Inc. Based at the company’s headquarters in Smithfield, Virginia, Leeth leads the company’s global sustainability strategies, which now focus on seven core pillars: animal welfare; diversity, equity and inclusion; environmental stewardship; food safety and quality; health and wellness; helping local communities and worker health and safety. He also leads Smithfield’s environmental compliance programs.

Leeth joined Smithfield Foods’ legal department in 2008 and served in a variety of legal, regulatory and government affairs roles with the company before being appointed to his current position in 2016. Under his leadership, the company has announced several industry-first carbon reduction goals, met its commitment to move pregnant sows into group housing on company-owned farms and exceeded its goal to source feed from farms utilizing precision farming techniques that reduce fertilizer use in the company’s supply chain. More recently, Smithfield has reported substantial progress toward its original GHG reduction target and has adopted even greater climate targets, including a 30% GHG reduction goal under the Science Based Targets initiative and a pledge to become carbon negative in all U.S. company-owned operations by 2030.

Prior to joining Smithfield Foods, Leeth was a partner at a major global law firm, where he represented the firm’s clients before federal and state courts and agencies in matters involving major federal and state environmental statutes, water rights disputes, cost recovery and contaminated property litigation, rulemaking and permitting. He also focused on state and local government matters and land-use disputes.

Leeth previously served as Assistant Attorney General for the Commonwealth of Virginia, representing a variety of state agencies, and began his legal career working as a law clerk to a federal judge presiding in U.S. District Court for the Eastern District of Virginia.

Dr. Jessica Agnew

Jessica Agnew holds a Ph.D. in Planning, Governance, and Globalization from Virginia Tech, specializing in International Development Planning. She also holds a Master of Public Health from Virginia Tech and a Master of Science in Food, Agriculture, and Resource Economics from the University of Guelph. As the managing editor for the Global Agricultural Productivity (GAP) Report® and co-lead of the GAP Initiative at Virginia Tech, she draws on a decade of experience working in emerging agricultural sectors and developing resilient, nutritious food systems to advocate for sustainable productivity growth. In addition to her role with the GAP Initiative, she serves as the Associate Director for the College of Agriculture and Life Sciences Global Programs at Virginia Tech. Agnew also has an active research portfolio on innovation for improving access to safe and nutritious foods through agri-food value chains and equitable markets and deploying digital technologies for agricultural sector transformation.

Dr. Wei Zhang

Wei Zhang is an assistant professor in the department of agricultural and applied economics at Virginia Tech. Her research focuses on the environmental and resource-use implications of agricultural production and the design of agri-environmental policy. Her ongoing research projects include climate change and agricultural productivity growth, benefits and costs of the USDA Environmental Quality Incentives Program, and on-farm loss and waste of vegetables in the United States.

Dr. Tom Thompson

Thomas L. (Tom) Thompson is Associate Dean and Director of Global Programs in the College of Agriculture and Life Sciences at Virginia Tech. CALS Global builds partnerships, drives thought leadership, and creates opportunities for students and faculty to serve globally. Thompson earned BS, MS, and PhD degrees in agronomy and soil science. He was department head at Virginia Tech (2011-16) and Texas Tech University (2006-11) and professor and extension specialist at the University of Arizona from 1991 to 2006. Thompson is also a Professor of Agronomy and has published more than 60 refereed journal articles and garnered more than $7 million in extramural funding. His recent research and outreach have focused on the adoption of conservation agriculture in smallholder farming systems in Haiti, Senegal, and Southeast Asia. He has mentored graduate students from Africa, Asia, and Central and South America. Under his leadership, the Global Agricultural Productivity Report (GAP Report) was awarded to Virginia Tech in 2019. The GAP Report tracks global trends in agricultural productivity and is launched annually in Washington, DC. Thompson has completed LEAD21 and the Food Systems Leadership Institute, two nationwide leadership development programs. He is a Fellow of the American Society of Agronomy and the Soil Science Society of America.

Dr. Cyril R. Clarke

A veterinarian, clinical pharmacologist, teacher, researcher, and distinguished academic leader, Dr. Cyril R. Clarke became the Executive Vice President and Provost of Virginia Tech in January 2019, after serving in an interim capacity since November 2017.

A native of Johannesburg, South Africa, Clarke earned his professional veterinary degree from the University of Pretoria, South Africa, a Ph.D. in veterinary pharmacology from Louisiana State University, and a master’s degree in higher education from Oklahoma State University. He is certified as a Diplomate of the American College of Veterinary Clinical Pharmacology.

Clarke’s initial faculty appointment in 1987 was at Oklahoma State University, where he also served as an academic department head and associate dean for academic affairs in the Center for Veterinary Health Sciences. Funded by corporate, state, and federal agencies, including the U.S. Department of Agriculture and National Institutes of Health, Clarke’s research focused on the interactions between antibacterial agents, animal patients, and infectious microbes. He is a recipient of the Pfizer Award for Research Excellence.

In 2007, Clarke was appointed to the position of Lois Bates Acheson Dean of the College of Veterinary Medicine at Oregon State University. During his time as dean, Clarke continued to teach pharmacology to veterinary students. In addition to receiving a Certificate of Excellence in Teaching, Clarke was honored with the Oregon Veterinary Medical Association’s President’s Award. He subsequently joined Virginia Tech in October, 2013, as Dean of the Virginia-Maryland College of Veterinary Medicine.

Clarke has held leadership positions in several professional organizations, including the board of directors for the Association of American Veterinary Medical Colleges and past president of the American College of Veterinary Clinical Pharmacology. He is also a past member of the National Agricultural Research, Extension, Education, and Economics Advisory Board and the AVMA Council on Education, the accrediting agency for veterinary medical education in North America.

Dr. Jewel Bronaugh

Dr. Jewel H. Bronaugh was appointed the 16th Commissioner of the Virginia Department of Agriculture and Consumer Services in 2018 by Governor Ralph Northam. She previously served as the Virginia State Executive Director for the USDA Farm Service Agency (FSA), appointed by Governor Terry McAuliffe and then-U.S. Secretary of Agriculture, Tom Vilsack, in July 2015. Prior to her FSA appointment, she served as Dean of the College of Agriculture at Virginia State University (VSU) with oversight of Extension, Research and Academic Programs. Previously she was the Associate Administrator for Extension Programs and a 4-H Extension Specialist.

In spring 2019, Dr. Bronaugh launched the Virginia Farmer Stress Task Force to raise awareness and coordinate resources to address farmer stress and mental health challenges in Virginia. In the fall of 2020, she helped establish the Virginia Food Access Investment Fund and Program, the first statewide program of its kind to address food access within historically marginalized communities.

Dr. Bronaugh received her Ph.D. in Career and Technical Education from Virginia Tech. She is passionate about the advancement of youth leadership in agriculture. Dr. Bronaugh is from Petersburg, Virginia. She is married to Cleavon, a retired United States Army Veteran.

Nancy Mungai

Nancy W. Mungai is a professor of soil science with research interests in biological nitrogen fixation in grain legumes, biological agricultural inputs, and relevance of soil-based approaches for adaptation & mitigation to climate change. She has successfully coordinated twelve research projects and several student internship programs. Nancy is currently involved in a project titled “Transforming African Agricultural Universities to meaningfully to contribute to Africa’s growth and development (TAGDev) a partnership of Egerton university with Gulu University funded by Mastercard Foundation through RUFORUM. The project has supported over 110 undergraduate and 110 postgraduate students to pursue various agricultural related disciplines including agronomy, horticulture, agribusiness and food nutrition and security. TAGDev has piloted an innovative model for agricultural training that facilitates agricultural students to work closely with rural communities to foster food system transformation. Community action research approaches have been at the center of TAGDev project implementation.

Nancy is also a member of a research consortium lead by Michigan State University dubbed “Sustainable Agricultural Intensification and Rural Economic Transformation (SAIRET+)” that is developing longer term proposal to support increased agricultural productivity through sustainable fertilizer use in Africa.

Nancy has supervised over 20 graduate students and has published 72 publications in internationally refereed and peer-reviewed journals, conference proceedings and technical reports.

Administratively, Nancy is the Ag. Director in charge of Research and Extension at Egerton University since March 2020. Previously she served as the Director in charge of undergraduate studies and field attachment programs for 9 years.

Jason Grant

Dr. Jason Grant is the W.G. Wysor Professor of Agriculture and Director of the Center for Agricultural Trade at Virginia Tech. Dr. Grant joined the Department of Agricultural and Applied Economics in 2007, after completing his Ph.D. at Purdue University. Dr. Grant has built an internationally recognized program in agricultural markets and trade at Virginia Tech, which includes planning and developing the annual Governor’s Conference on Agricultural Trade through a partnership with four other State agencies across the Commonwealth of Virginia. Dr. Grant is passionate about teaching students to be “job ready” and thinking “globally” as they enter careers in agricultural industries. His research investigates key trends in global markets shaping U.S. commodity production and export, including the impacts of trade disputes, retaliatory trade actions, SPS issues, Codex food safety standards, competitive regionalism, and adaptation to extreme climate events. He has previously served as guest editor of Choices, leading a team of USDA policymakers and academics to assess the economic impacts of the 2018/19 trade dispute and retaliatory trade actions impacting U.S. agriculture. In 2021, this work was recognized by the American Agricultural and Applied Economics Association (AAEA) for the profession’s outstanding Choices article award for outreach contribution. In 2020, he was the recipient of USDA’s Bruce Gardner Award for outstanding contributions by an outside Economist shaping U.S. government programs and policies, and has previously been the recipient of the AAEA’s Honorable Mention award for Outstanding Journal Article; the European Agricultural Economics Association’s Quality of Policy Contribution Award for his work on international trade agreements; and the 2018 APEX award from Purdue University’s Department of Agricultural Economics which recognizes outstanding contributions by an alumni. Dr. Grant currently serves as associate editor of the American Journal of Agricultural Economics.

Florah Kirira

Florah joined Farm Input Promotions Africa (FIPS) just after college, in 2013 as a monitoring and evaluation officer.

After two years, she was promoted to lead training, which included development of training curriculums and deploying the curriculum to farmers and trainers of trainers.

Florah has also coordinated programs within FIPS such as youth work and potato work.

Currently, she leads the partnership development work that includes developing new relationships, developing ideas for funding, and maintaining existing relationships, among other roles.

Folu Okunade

Folu serves as the Chief Operating Officer for Hello Tractor, responsible for shaping, executing and measuring the organization’s growth strategy and operations. Prior to joining Hello Tractor in 2019, Folu served as Senior Manager at Accenture focused on defining and implementing large-scale transformational process improvement solutions, primarily within the financial services sector. Folu’s experience extends to driving agricultural systems change at the NEPAD Business Foundation, specifically within the continental agriculture program (CAADP). Folu holds a Master of Business Administration (MBA) from the University of Cape Town (specializing in Leadership and Doing Business in Africa) and a Bachelor of Science degree in Economics from Washington University in St. Louis. Folu’s professional interests lie at the intersection of macroeconomic growth, impact entrepreneurial empowerment, strategic organizational alignment, and technology-led social innovations.

Tim Njagi

Tim Njagi is a seasoned Development Economist with a wealth of 15 years of experience in the fields of development planning, policy implementation and research. He holds a PhD in Development Economics and Master’s Degree in International Development from the National Graduate Institute for Policy Studies (GRIPS), Japan.

He has experience working in the public sector having worked with the National Treasury and Planning in Kenya and is currently a Fellow with Tegemeo Institute of Agricultural Policy and Development of Egerton University.

His current research focus is on farm productivity, technology adoption, irrigation, governance, resilience and impact evaluation., irrigation, credit, governance, land issues, and resilience, where he has a number of publications.

He is also a member of the International Association of Agricultural Economists (IAAE), African Association of Agricultural Economics (AAAE), African Evaluation Association (AfREA), Evaluation Society of Kenya (ESK), and the Institute of Economic Affairs (EIA) in Kenya.

He aspires to make a significant contribution towards addressing food insecurity and poverty in developing countries.

Isaac Kibwage

Isaac Kibwage is currently the Vice-Chancellor of Egerton University. He has variously initiated and/or guided development and implementation of the strategic plan for 2018-2023 and policies of the University.

Isaac Kibwage is on leave of absence from the University of Nairobi where he serves as a Professor of Pharmaceutical Chemistry in the School of Pharmacy. He has published widely in his discipline.

During May 2007- May 2017, Isaac Kibwage served as the Principal of College of Health Sciences, University of Nairobi where he was the Academic Research, Financial and Administrative head of the college. The College comprises the Schools of; Medicine, Pharmacy, Dental Siences, Nursing Sciences and Public Health, the University of Nairobi Institute of Tropical and Infectious Dieases, KAVI-Institute of Clinical Research, the East Africa Kidney Institute and the Centre for HIV/Aids Research and Prevention. He was responsible for all research activities at the College ensuring compliance to project objectives and prudent utilization of resources per approved budgets. Isaac Kibwage handled College responsibilities and guided its expansion and excellent performance culminating in it being awarded a Shield as ”Center of Excellence in the Health Sciences” by the East African Community in 2014. Further, research funding grew about four times and the College had a continuous level of ‘Excellent performance’ in performance contracting amongst the six colleges of the University.

Isaac Kibwage has held various positions in the Pharmaceutical Society of Kenya including the Chairmanship for a period of 6 years. He has broad experience in the pharmaceutical regulatory systems locally and internationally, and specifically in the quality control and quality assurance of medicines. Due to his commitment and exemplary pharmaceutical services, Isaac Kibwage was awarded the “Head of State Commendation“ and the Pharmaceutical Society of Kenya conferred on him the title of “Fellow of the Pharmaceutical Society of Kenya.”

Canisius Kanangire

Dr. Canisius Kanangire is the Executive Director at AATF. He previously was the

Executive Secretary of the African Ministers’ Council on Water. He has held other positions including, Executive Secretary of the Lake Victoria Basin Commission; Regional Manager for Capacity Building and Head of Strategic Planning and Management at the Nile Basin Initiative; Lecturer and Dean – Faculty of Agriculture, University of Rwanda.

He holds a PhD and MSc in Aquatic Sciences from the University of Namur (Belgium), a Degree in Biology majoring in Environmental Sciences, and an Undergraduate Certificate in Biology and Chemistry from the “Institut Supérieur Pédagogique de Bukavu.

Nassib Mugwanya

Nassib Mugwanya is Manager of Global Partnerships – Agriculture Engagement & Activation at Bayer and leads the smallholder farmer engagement within the Global Stakeholders Affairs & Strategy Partnerships team. Prior to joining Bayer, Nassib worked with the National Agricultural Research Organization in Uganda, where he spent most of his time in educational and outreach engagements on biotechnology among smallholder farmers. Nassib has a background in agriculture, with a doctorate in agricultural extension and education from North Carolina State University, and a BSc and MSc in agriculture and extension education from Makerere University-Kampala.

Humphrey Kiruaye

Humphrey joined DuPont Pioneer in 2015 as a Marketing Leader for Eastern Southern Central Africa Region. In 2016, he was appointed the Commercial leader for Kenya responsible for the Pioneer and Pannar Seed brands.

In 2017, he was appointed to his current role as Country Leader/Director for Corteva Agriscience Kenya and Greatlakes Countries (Uganda, Rwanda, Burundi & DRC).

Prior to joining Pioneer, Humphrey worked at Syngenta AG for 10 years in various roles; Business Manager for Smallholder Segment, Marketing Manager Strategy and planning, Area Sales Manager amongst other roles.

Education Background:

Masters Business Administration (Strategic Management), The University of Nairobi.

Bachelor of Science Degree in Horticulture, Egerton University.

Benson Mutuku

Benson Mutuku is development and humanitarian professional with over 13 years of experience working with INGOs, NGOs, the private sector, and government institutions. Benson has extensive experience in programmatic design, implementation, and technical advising of gender programs in Agriculture, Food Security and Nutrition, Financial Inclusion & Economic Empowerment, Policy and Advocacy, and Education and Health. Benson has spearheaded and provided technical expertise in multi-country projects in Kenya, Rwanda, Uganda, Djibouti, Tanzania, Mozambique, Ethiopia, Burundi, Zambia, Somalia, Ghana and Uganda. Benson has worked on various policy related initiatives and research activities. He is experienced in monitoring and evaluation hence providing oversight for a program’s planning, evaluation, knowledge management and monitoring. Benson is a seasoned trainer both at the community level as well as at the policy level, having engaged in capacity building processes across the country and beyond. Benson has basic French speaking skills. Benson is passionate about gender transformation at the local, national, regional, and other spheres of influence.

Okeyo Mwai

Ally Okeyo Mwai is Principal Scientist in the ILRI’s Global Livestock Genetics- Live Gene Research Program. Okeyo is a quantitative geneticist with over 30 years of experience in practical design and implementation of livestock improvement programs in sub-Saharan Africa and South Asia regions. Okeyo has in the past led ILRI’s Breeding strategies Research, specifically focusing on development and implementation projects, covering a wide range of research areas including, characterization and genetic diversity of indigenous tropical livestock; their improved utilization, as well as development and application of assisted reproductive technologies in dairy cattle. Prior to joining ILRI, he was head of the Animal Breeding and Genetics Section at the Department of Animal Production, University of Nairobi and Coordinator of Small Ruminant Research Program at the then Kenya Agricultural and Livestock Research organization. Okeyo has and holds several national and international advisory board positions. He is currently leading the development of ILRI led dairy cattle genetic gain development and research programs in eastern Africa region. Okeyo has published extensively (authored and co-authored more than 150 scientific journal and conference papers), and has held several scientific editorials, and national and international advisory board positions. Okeyo holds MSc Animal Science (Animal Genetics) from University of California, Davis and a PhD in Animal Breeding and Genetics from University of Nairobi.

Tony Fernandes

Tony Fernandes became Deputy Assistant Secretary of State for Trade Policy and Negotiations in the Bureau of Economic and Business Affairs in March 2022, after having served as Acting Deputy Assistant Secretary since August 2021.

Prior to that, Tony was Director of the Multilateral Trade Affairs Office in the Bureau of Economic and Business Affairs at the U.S. Department of State.

Previously, Tony was Director for Regional Affairs in the Bureau of Legislative Affairs and Director for Africa and Middle East Programs in the Bureau of International Narcotics and Law Enforcement Affairs. He also served in the Office of the United States Trade Representative, the Diplomatic Readiness Task Force, and the Operations Center. His overseas assignments include positions in Turkey, Nigeria, Russia, Canada, and China.

Tony joined the Foreign Service in 1997 and is a member of the Senior Foreign Service.

He holds a B.A. from Boston College, a J.D. from the University of Minnesota School of Law, and a Master’s in National Security Strategy from the National War College.

Karen Hulebak

Karen Hulebak is a consultant working primarily on Codex Alimentarius matters. She has 20+ years of experience with Codex, having chaired the Codex Committee on Food Hygiene for 7 years, served as Vice Chair of the Commission for two terms (2005-2008) and as Chairperson of the Commission for two terms (2008-2011). Prior to her election as Codex Chairperson, she served as USDA/FSIS Chief Scientist, and as Assistant Administrator for the FSIS Office of Public Health Science. She has an Sc.D. in toxicology from the Johns Hopkins University School of Public Health.

Ann Steensland

Ann Steensland leads the GAP Report Initiative for CALS Global at the Virginia Tech College of Agriculture and Life Sciences. In this role, she serves as the lead author of the Global Agricultural Productivity Report, or GAP Report, an annual analysis of global progress toward productive sustainable food and agricultural systems. Her research areas include sustainable approaches for increasing the productivity of small-scale agriculture, improving livelihoods for small-scale farmers, and connecting small-scale and emerging farmers to markets. Prior to joining Virginia Tech, Ms. Steensland was the Deputy Director of the Global Harvest Initiative and the Chief of Staff of the Alliance to End Hunger. Ms. Steensland has a B.A. in International Relations and an M.A. in African History. She was awarded the Lawrence Levine Prize for her M.A. thesis exploring racial, political, and environmental aspects of the commercialization of agriculture in South Africa.

Dr. Siboniso Moyo

Siboniso “Boni” Moyo is deputy director general for research and development at the International Livestock Research Institute. Between 2015 and 2016, she was program leader of ILRI’s animal science for sustainable productivity program. From 2006−2014, Dr. Moyo was ILRI’s regional representative in Southern Africa. She has 25 years’ experience conducting livestock research and development in Zimbabwe and southern Africa. Her fields of specialization include breed performance evaluation, livestock production systems, livestock research and management, and partnership development. Dr. Moyo has an MSc in animal husbandry from the Patrice Lumumba University in Moscow and a PhD in animal science from the University of Pretoria. Before joining ILRI she was National Director for Livestock Production and Development in Zimbabwe (2002–2005).

Dr. Jim Gaffney